Articles, books, and presentations periodically come to our attention we think business owners and their advisors ought to find valuable. This presentation is one of those. Review time is estimated to be about 20 minutes. Thinking time may be much longer.

Have you read AI Super-Powers: China, Silicon Valley, and the New World Order?

Answer: If you are a business owner or an advisor to business owners I strongly suggest you buy Kai-Fu Lee’s recently published book[1], read it, and carefully reflect on what you read in the contexts of business value, business transition, and how much different our world is likely to be when near- and longer-term AI related changes are virtually certain to occur ‘before our very eyes’.

What is meant by the term artificial intelligence?

Answer: Artificial intelligence (AI) is an umbrella term used to describe the ability of a mechanical device (e.g. a computer or computer-controlled robot) and related programming and systems endowed with the ability to reason, discover meaning, generalize, self-correct, and – importantly in the context of deep learning – learn from past experience.

What is meant by the artificial intelligence term ‘deep learning’?

Answer: Deep learning is a term used to describe the use of computer algorithms to progressively manipulate large amounts of data to generate otherwise unobtainable, useful outputs that can be used to improve both commercial and non-commercial results.

Deep learning through algorithmic activity may prove to be the greatest business game changer of all – and hence to business-specific prospective value and in business-specific transition contexts.

Who is Kai-Fu Lee, and what does he know about artificial intelligence?

Answer: Dr. Kai-Fu Lee is the chairman and CEO of Sinovation Ventures[2], a China-based venture capital firm. Educated in the United States, prior to founding Sinovation Ventures he was President of Google China having previously held U.S. executive positions with Apple, SGI and Microsoft. Lee is said to be:

one of the world’s most respected experts on Artificial Intelligence and on China.

an oracle when it comes to predicting the future of technology in China.

A former Apple CEO likens Lee’s explanation of the ‘new AI world order’ to Steve Jobs early explanation of how personal computing would fundamentally change humanity.

See Dr. Kai-Fu Lee interviewed on CBS’s 60 Minutes earlier this year.

In 149 words, why should I read AI Super-Powers?

Refined Answer: Among many other things, Lee explains in his book why he believes:

AI will advance quickly and exponentially.

AI will create U.S. and China dominance, where the U.S. and China are culturally different.

AI will result in job losses and in growing inequality both between and within countries.

AI, in particular ‘deep learning’, will revolutionize dozens of industries. Business owners and their advisors need to read Lee’s book, and then interpolate what AI is likely to mean – both directly and indirectly – to their businesses, those of their clients, and to business value and transition options.

Chinese government officials, entrepreneurs, and investors are “ramping up AI investment, research, and entrepreneurship on a historic scale”.

Recent, powerful developments tip the balance of AI power in China’s direction.

Crass Answer: If you have to ask you probably shouldn’t. Instead, have fun until you don’t.

One Minute Survey

Time's up

[1] Available at Amazon, Apple, and likely at your favorite bookstore.

[2] From the Sinovation Ventures website – August 2019: Sinovation Ventures is an established Chinese technology-savvy investment firm, started in 2009 by a team led by Dr. Kai-Fu Lee, with presence in Beijing, Shanghai, Shenzhen, Seattle and Silicon Valley. We currently manage an over $2B AUM between seven USD and RMB funds in total, and over 300 portfolio companies across the technology spectrum in China and the U.S. We are one of the first Chinese ventures firms establishing a presence and investment practice in the U.S.

Why is a picture of Charles Darwin[1]relevant to a discussion of business value and transition?

Answer: Based on 50 years of business value and transition consulting experience I believe:

we live in a watershed economic, business, and business value and transition environment.

today, as never before, Charles Darwin’s thesis of natural selection needs to be understood and considered by every business owner.

What is Charles Darwin’s thesis of natural selection?

Initially, Darwin did not use the term Survival of the fittest. Instead, British economist Herbert Spencer used that phrase after reading Darwin’s 1859 book On the Origin of Species. It caught on, and Darwin used the term in a subsequent edition of his book.

Survival of the fittest is an umbrella phrase that masks and leads many to misinterpret Darwin’s messaging. If one takes the time to read and consider other quotes attributed to Darwin[2] it becomes clear that a high level Darwin’s thesis can be stated to be:

‘those who implement change to their advantage more quickly than others are those who, through collaboration, best identify and adapt to change.’

Is ongoing economic and business change impacting business value and transition?

The answer must be ‘yes’ given the smorgasbord of ongoing inter-related economic and business-related segment changes that include:

Globallization.

Potential de-globalization if President Trump has his way.

Central bank policies – particularly after 2008.

Developed and developing country government debt, government intervention, government policies, and government intervention.

Technological advances.

Business consolidation.

Financial markets heavily influenced by algorithmic trading.

Climate change.

World population growth and societal disruption.

Incomplete, sensationalized, and in some cases what appears to be poorly researched news.

These and other things will continue to impact both the value and transition of most if not all large and small publicly and privately-owned businesses to varying positive and negative degrees.

Concerning that melded ongoing change:

Some of these changes and related changes are more predictable than others.

The pace of change is likely to escalate in some of the cited segments.

All businesses will be influenced in varying degrees and for better or worse by ongoing changes.

For some companies these changes collectively may lead to business value enhancement, for others business value deterioration – and hence to greater or less business transition success.

How does Darwin’s thesis play into a discussion of business value and transition?

Business value growth and in turn successful business transition are both influenced – I believe in an ever-escalating way – by the degree to which business owners accept and act upon Darwin’s thesis.

It is crucial that all business owners hear this messaging, and that each decide whether they agree it makes sense. Moreover, this messaging is particularly important for owners of family businesses. That is because there is a greater proclivity for family business owners to compromise from arm’s length principles where their emotional intelligence plays too large a part in their business decision making.

I believe that all business owners should consider Darwin’s thesis and apply it to their specific circumstances. Private company business owners, irrespective of whether the business is family-owned, need to consider their ability to adapt quickly to changing business conditions and prospects having regard to their collective capabilities and the current and prospective financial position of their company.

Private company business owners should consider now – and on an ongoing basis as they experience continuing change in our increasingly competitive business environment:

whether developments and advances outside their control are impacting the near- and long-term risks and going-concern viability of their business.

whether the long-term going-concern viability of their business is at risk as a result of its current financial position, growth prospects, and competitive prospects going forward.

whether the size and prospective size of their business are such that it will be able to compete effectively in the near- and long-term. This where larger companies in many cases seem increasingly likely to be favored in the contexts of – among other things – both supply and demand chain metrics as a result of ongoing globalization and technology advances and the costs and cost savings related to both of those things.

whether as a result of conclusions reached in respect of business viability and likely future competitiveness, whether their business should be offered for sale now, or be prepared for sale at some point in the next, say, two – five years.

whether current employees need to be replaced with persons better equipped to face current and prospective competitive challenges.

whether ongoing technological advances may have a material favorable or adverse effect on their business in the contexts of both required future capital investment, and the timing of that investment.

Finally, in family businesses, it is becoming ever more critical to consider whether employed family members should retain their current positions, or should assume jobs that better suit their skill sets. Any family business owner that objectively makes such assessments and acts on them will bring a smile to Charles Darwin’s face, wherever he now is.

[1] Charles Darwin’s (1809 – 1882) book On the Origin of Species by Means of Natural Selection, or the Preservation of Favoured Races in the Struggle for Life was first published in 1859.

[2] For example, Darwin is quoted as saying: “It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one most adaptable to change, that lives within the means available and works co-operatively against common threats.” ”The world will not be inherited by the strongest, it will be inherited by those most able to change.” “It is not the biggest, the brightest or the best that will survive, but those who adapt the quickest.” “In the long history of humankind (and animal kind, too) those who learned to collaborate and improvise most effectively have prevailed.”

How Necessary is Good Corporate Governance to Business Value Growth and Business Transition Success?

Answer: Very necessary! It is not a stretch to suggest that for privately-held companies it is a fair generalization to suggest that business value growth and business transition success on the one hand, and corporate governance on the other, are interdependent. Further, at any given point in time assessing the veracity of a company’s corporate governance is fundamental to developing either its notional value or negotiating an open market price for all of its outstanding shares.

Commentary: We live in a business and social environment evermore influenced by continual transitioning globalization factors, central bank policies, government-related business and societal uncertainties, ongoing technological advances, and ongoing business combinations activity. It follows that Implementation and ongoing compliance with superior corporate governance practices are increasingly important to promote ongoing viability, value growth and successful ownership transition in individual private companies. See related blog posts Business Transition – General: The Right Overview Question and Recession Impact by Industry and Business is a ‘Right Question’! .

Why a Chrysalis -> Butterfly image?

Question: Why a chrysalis -> butterfly image as a lead-in to a discussion of corporate governance?

Answer: We live today in a world of continual transition on many important fronts. If the butterfly does not react to climate change and hence does not successfully transition from its chrysalis state, it will not survive. Parallels in this regard between the butterfly and a privately-owned company are very easy to identify.

What is Corporate Governance?

Answer: Corporate governance is a term used to describe the system of mechanisms and processes by which a business is controlled and directed. Broadly, a corporate governance system:

details the rights and responsibilities of the board of directors, members of an advisory board if one exists, owners, executives, managers, and other employees.

establishes and continually adjusts the rules, practices, and processes:

that influence and appropriately align and balance the mutual and individual interests of all stakeholders.

for making business decisions.

that collectively coordinate and monitor the company’s objectives through strategic plans, business plans and forecasts, and the like.

Ensures all of those things are complied with on an ongoing basis through a continuous monitoring process.

Corporate Governance Initiatives. Which Should Private Company Owners Prioritize?

Answer: If corporate governance excellence is absent in their company, business owners should:

consider engaging an independent, objective consultant with experience in their industry to conduct a detailed Strengths, Weaknesses, Opportunities, and Threats (SWOT) analysis of their business.

based on that SWOT analysis, decide whether the business:

is likely to be viable as a going concern In the long-term, or

should be organized for sale to an arm’s length purchaser.

if the business is assessed as likely to be viable as a going concern in the long-term:

identify recently retired (preferably same-industry) executives or other qualified people and invite them to join the company’s board of directors.

alternately, establish an advisory board of such arm’s length people if candidates are not willing to accept the fiduciary responsibilities director’s shoulder – or if an advisory board is a preferred course.

If a family business, elect a non-family member as Chairperson of the Board or Advisory Committee as the case may be.

make that Chairperson responsible for developing, implementing, and thereafter monitoring, a sound corporate governance system for your company going forward.

Important Corporate Governance Comment

There are advisors, be they directors, business advisors or professional advisors – and then there are advisors. A business owner should only engage advisors where mutual respect and trust exists, and where the advisors ‘speak truth to power’ – and are listened to and not resented for doing that. I am particularly emphatic on these things in the case of family business owners who employ family members.

Question: Why the Rusty Can and a focus on Recession?

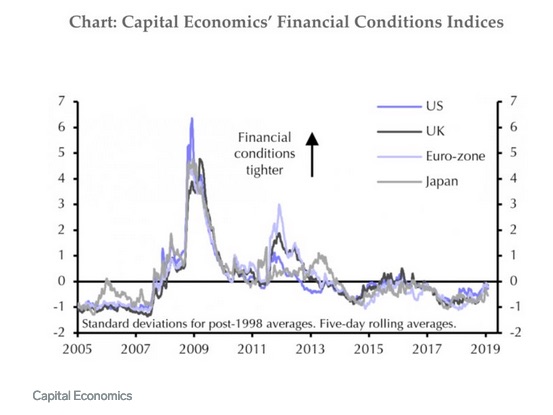

Answer: I and many others believe that central bank quantitative easing after September 2008 has proven to be a ‘kick the can down the road’ exercise that, combined with government debt, government regulation, government trade policies, ongoing technological advances, slowing economic growth in a number of countries, ongoing Brexit non-negotiations, ongoing societal change and climate change – along with other things – will contribute to a global recession in the near-term.

Recently when considering a Strengths, Weaknesses, Opportunities, and Threats (SWOT) business analysis that landed on my desk I decided to research the question of the variable impacts of a recession on different industries and businesses. I was able to find limited very high-level commentary on those things. However, much to my surprise I was unable to find any helpful high-level analysis of underlying business structure factors that tend to lead to a greater or lesser recession impact on any given industry or business.

If you are reading this and know of any such analysis, please add a comment to this post directing me and other readers to it.

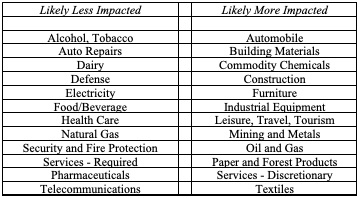

Question: What principal factors determine which industries are least and most likel impacted by a recession?

Answer: Based on my over fifty years’ experience, I believe two things viewed in isolation significantly contribute to which industries – and specific businesses within those industries – are most and least impacted by a recession. These are:

which government programs are likely to be prioritized – through necessity or due to political perceptions – during a recessionary period, and which are not.

which products are ‘consumer necessities’, which are less ‘consumer necessary’, and which are not ‘consumer necessary’. The further along that spectrum is an industry – or better yet the products or services of an individual business – the more ought to be the recessionary impact.

The following is a sample of supplier, manufacturer, wholesaler, retailer, and supply chain management participants I think can reasonably be categorized as likely to be ‘less’ and ‘more’ impacted by a recession.

It is necessary to focus on each industry and every business individually when considering recession-vulnerability. For example, the types of goods they transport and the services they offer influence the recession experience of supply-chain companies where:

a food wholesaling business may be impacted less or more by recession depending on the food manufacturers they represent.

a trucking business may be less impacted by inflation if it principally services food and beverage manufacturers, wholesalers and retailers as contrasted with one that predominantly services automotive manufacturers.

First: “We expect the classic cyclical commodity industries and those industries that support them to be most severely impacted (by recession). Examples include forestry and building products, oil and gas exploration and production, oil and gas services, mining, commodity chemicals and industrial machinery. Trucking, construction and engineering will also be hit to varying degrees depending on their end markets. The common theme with these industries is their relative capital intensity and high fixed expenses.”.

Second: “There is a clear, three-step process that recession winners follow:

They stress test their businesses by modeling recession scenarios and studying the impacts on several factors, including their liquidity, operations and competitive position;

They are very clear on their winning formula; and

They have a playbook to match each recession scenario that they have studied.”

Third: “Ample financial liquidity, that is cash that the business can access under various economic conditions, underpins a company’s ability to capitalize on a recession.”

I suggest a third article, A Mixed Economic Bag in 2019 by Nouriel Roubini is also worth reading. Roubini is the New York University economist who rightly predicted the 2008 Great Recession.

If business owners currently are not planning for a recession they should be. Their advisors need to take this idea to their business owner clients now and not later.

Note: Paris Aden is the founding partner of Valitas Capital Partners, a M&A Advisory Business based in Toronto, Canada. TEC Canada published Mr. Aden’s article. TEC Canada facilitates the formation of business owner peer groups supported by one-to-one coaching, expert speakers, education and global networking.

I suggest the number one ‘right’ question business owners and their advisors need to ask today is: Does your business currently have a strong enough balance sheet to enable it to survive and prosper through at least two years of recession?

Prior to readers answering that question in the context of any given business, I further suggest they focus and reach conclusions on the following supplemental questions:

Does your business have unused borrowing capacity available if funding to bridge a business downturn is required?

Does your business own assets redundant to its operations that could be liquidated if necessary?

Can your business significantly improve its operating discretionary cash flow by achieving labor, material, overhead or other cost savings within its current cost structure?

Does your business have well-maintained capital equipment that will not necessitate large capital expenditures in the foreseeable future as a result of un-remedied wear and tear?

Irrespective of the state of maintenance of the current capital equipment of your business will your business likely face major capital equipment requirements as a result of ongoing technological advances?

If your business is likely to face technology-related major capital equipment requirements is the timing of that spend going to occur earlier than you previously anticipated?

Does your business have significant contingent environmental, unfunded pension or other liabilities that may negatively affect its long-term viability?

Is your business subject to declining operating margins and after-tax discretionary cash flow in an increasingly competitive business environment?

Answer/Commentary

In our current and prospective economic, business and societal environment for most businesses continual review of balance sheet strength needs to be a, if not the top business owner priority. This where balance sheet strength at any given point in time means in:

the first instance that a business has an adequate yet efficient level of working capital to meet its business plan.

the second instance means that a business is not over-levered. That is, the business does not owe more than an appropriate amount of third-party interest-bearing debt given its asset base and its current and expected annual operating before- and after-tax discretionary cash flow.

the third instance ensuring a business is financially positioned to be able to survive significant both anticipated and unanticipated external and internal economic, industry, and company-specific events.

In our current environment, I suggest the importance of balance sheet strength can’t be underrated. This given prevailing economic, business and financial markets uncertainty that follows from, along with other things:

We have not experienced a period of recession (defined by economists as two consecutive quarters of gross domestic product growth decreases) in most of the developed countries for over a decade. It is virtually certain that we will face recession at some point. This where history and current economic indicators suggest for many that recession will come sooner than later, but inevitably will come.

Ongoing globalization issues, threats of de-globalization, continual government bickering over and disruption to international trade agreements and tariffs – principally emanating from the U.S. Oval Office policies, arguably have taken on a life of their own.

Increasing evidence that Central Bank so-called quantitative easing policies introduced in and after 2008 are not generating central bank anticipated economic growth in many countries.

The U.S. currently accounts for about 25% of world gross domestic product. Disruptive and polarized U.S. politics and polarized international and national policies largely emanating out of the White House, combined with the continual “Mueller cloud” that hangs over Mr. Trump’s Presidency, are economically and societally disturbing within the U.S. and elsewhere.

Government debt in many developed countries including the U.S. and Canada continues to escalate with no end in sight. I suggest that in particular this cumulative debt escalation, required infrastructure updates, climate change, and escalating societal issues inevitably must result in increased government regulation, increased business taxes, and other increased monetary levies on both privately- and publicly-held businesses.

Business consolidation in most industries continues apace. this threatens many smaller companies as large companies enjoy efficiencies as a result of critical mass, changes to supply (inputs) and distribution chain management, and a greater opportunity than smaller companies will have to exploit new and advancing technologies to their advantage.

Ongoing technological advances that many believe will result in significantly increased unemployment and societal disruption. If you haven’t read the 2013 Oxford University Study titled The Future Of Employment: How Susceptible Are Jobs To Computerization I suggest you do that.

An environment where if financial institutions were deemed ‘too big to fail’ in 2008 they are in 2019 even bigger and more influential. This where those financial institutions influence, if not as a practical matter control – the equity trading and investment markets.

In summary, I suggest business owners need to focus on the current and prospective efficacy of the balance sheet of their respective businesses – preparing for the worst while hoping for the best.

RSS - Posts

RSS - Posts