Articles, books, and presentations periodically come to our attention we think business owners and their advisors ought to find valuable. This presentation is one of those. Review time is estimated to be about 20 minutes. Thinking time may be much longer.

Question: Who is James Bullard, and what did he say yesterday?

Answer: James Bullard is the President and CEO of the Federal Reserve Bank of St. Louis, one of the twelve independent U.S. Regional Reserve Banks These are intended to ensure that when making U.S. national monetary policy economic conditions throughout the United States are considered.

Yesterday, August 6, Mr. Bullard addressed the National Economists Club in Washington, D.C. His presentation is titled A Sea Change in U.S. Monetary Policy. It is short and to the point. I believe business owners, their advisors, politicians, and anyone else interested in the global and country-specific economies ought to read and think about its contents.

Question: What topics does Mr. Bullard address that influence monetary policy?

Answer: Topics addressed (in alphabetic order) include:

Federal (Reserve) Open Market Committee (FOMC) policy.

Question: Why the Rusty Can and a focus on Recession?

Answer: I and many others believe that central bank quantitative easing after September 2008 has proven to be a ‘kick the can down the road’ exercise that, combined with government debt, government regulation, government trade policies, ongoing technological advances, slowing economic growth in a number of countries, ongoing Brexit non-negotiations, ongoing societal change and climate change – along with other things – will contribute to a global recession in the near-term.

Recently when considering a Strengths, Weaknesses, Opportunities, and Threats (SWOT) business analysis that landed on my desk I decided to research the question of the variable impacts of a recession on different industries and businesses. I was able to find limited very high-level commentary on those things. However, much to my surprise I was unable to find any helpful high-level analysis of underlying business structure factors that tend to lead to a greater or lesser recession impact on any given industry or business.

If you are reading this and know of any such analysis, please add a comment to this post directing me and other readers to it.

Question: What principal factors determine which industries are least and most likel impacted by a recession?

Answer: Based on my over fifty years’ experience, I believe two things viewed in isolation significantly contribute to which industries – and specific businesses within those industries – are most and least impacted by a recession. These are:

which government programs are likely to be prioritized – through necessity or due to political perceptions – during a recessionary period, and which are not.

which products are ‘consumer necessities’, which are less ‘consumer necessary’, and which are not ‘consumer necessary’. The further along that spectrum is an industry – or better yet the products or services of an individual business – the more ought to be the recessionary impact.

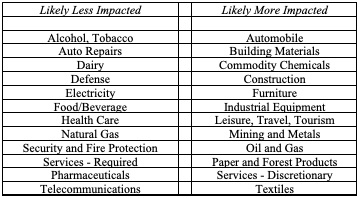

The following is a sample of supplier, manufacturer, wholesaler, retailer, and supply chain management participants I think can reasonably be categorized as likely to be ‘less’ and ‘more’ impacted by a recession.

It is necessary to focus on each industry and every business individually when considering recession-vulnerability. For example, the types of goods they transport and the services they offer influence the recession experience of supply-chain companies where:

a food wholesaling business may be impacted less or more by recession depending on the food manufacturers they represent.

a trucking business may be less impacted by inflation if it principally services food and beverage manufacturers, wholesalers and retailers as contrasted with one that predominantly services automotive manufacturers.

First: “We expect the classic cyclical commodity industries and those industries that support them to be most severely impacted (by recession). Examples include forestry and building products, oil and gas exploration and production, oil and gas services, mining, commodity chemicals and industrial machinery. Trucking, construction and engineering will also be hit to varying degrees depending on their end markets. The common theme with these industries is their relative capital intensity and high fixed expenses.”.

Second: “There is a clear, three-step process that recession winners follow:

They stress test their businesses by modeling recession scenarios and studying the impacts on several factors, including their liquidity, operations and competitive position;

They are very clear on their winning formula; and

They have a playbook to match each recession scenario that they have studied.”

Third: “Ample financial liquidity, that is cash that the business can access under various economic conditions, underpins a company’s ability to capitalize on a recession.”

I suggest a third article, A Mixed Economic Bag in 2019 by Nouriel Roubini is also worth reading. Roubini is the New York University economist who rightly predicted the 2008 Great Recession.

If business owners currently are not planning for a recession they should be. Their advisors need to take this idea to their business owner clients now and not later.

Note: Paris Aden is the founding partner of Valitas Capital Partners, a M&A Advisory Business based in Toronto, Canada. TEC Canada published Mr. Aden’s article. TEC Canada facilitates the formation of business owner peer groups supported by one-to-one coaching, expert speakers, education and global networking.

RSS - Posts

RSS - Posts