Question: Why the Rusty Can and a focus on Recession?

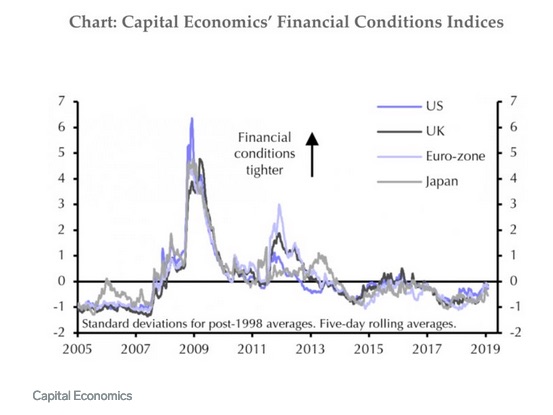

Answer: I and many others believe that central bank quantitative easing after September 2008 has proven to be a ‘kick the can down the road’ exercise that, combined with government debt, government regulation, government trade policies, ongoing technological advances, slowing economic growth in a number of countries, ongoing Brexit non-negotiations, ongoing societal change and climate change – along with other things – will contribute to a global recession in the near-term.

Recently when considering a Strengths, Weaknesses, Opportunities, and Threats (SWOT) business analysis that landed on my desk I decided to research the question of the variable impacts of a recession on different industries and businesses. I was able to find limited very high-level commentary on those things. However, much to my surprise I was unable to find any helpful high-level analysis of underlying business structure factors that tend to lead to a greater or lesser recession impact on any given industry or business.

If you are reading this and know of any such analysis, please add a comment to this post directing me and other readers to it.

Question: What principal factors determine which industries are least and most likel impacted by a recession?

Answer: Based on my over fifty years’ experience, I believe two things viewed in isolation significantly contribute to which industries – and specific businesses within those industries – are most and least impacted by a recession. These are:

which government programs are likely to be prioritized – through necessity or due to political perceptions – during a recessionary period, and which are not.

which products are ‘consumer necessities’, which are less ‘consumer necessary’, and which are not ‘consumer necessary’. The further along that spectrum is an industry – or better yet the products or services of an individual business – the more ought to be the recessionary impact.

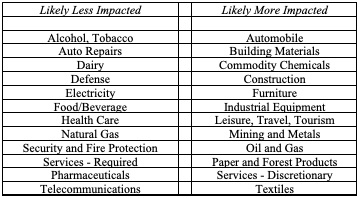

The following is a sample of supplier, manufacturer, wholesaler, retailer, and supply chain management participants I think can reasonably be categorized as likely to be ‘less’ and ‘more’ impacted by a recession.

It is necessary to focus on each industry and every business individually when considering recession-vulnerability. For example, the types of goods they transport and the services they offer influence the recession experience of supply-chain companies where:

a food wholesaling business may be impacted less or more by recession depending on the food manufacturers they represent.

a trucking business may be less impacted by inflation if it principally services food and beverage manufacturers, wholesalers and retailers as contrasted with one that predominantly services automotive manufacturers.

First: “We expect the classic cyclical commodity industries and those industries that support them to be most severely impacted (by recession). Examples include forestry and building products, oil and gas exploration and production, oil and gas services, mining, commodity chemicals and industrial machinery. Trucking, construction and engineering will also be hit to varying degrees depending on their end markets. The common theme with these industries is their relative capital intensity and high fixed expenses.”.

Second: “There is a clear, three-step process that recession winners follow:

They stress test their businesses by modeling recession scenarios and studying the impacts on several factors, including their liquidity, operations and competitive position;

They are very clear on their winning formula; and

They have a playbook to match each recession scenario that they have studied.”

Third: “Ample financial liquidity, that is cash that the business can access under various economic conditions, underpins a company’s ability to capitalize on a recession.”

I suggest a third article, A Mixed Economic Bag in 2019 by Nouriel Roubini is also worth reading. Roubini is the New York University economist who rightly predicted the 2008 Great Recession.

If business owners currently are not planning for a recession they should be. Their advisors need to take this idea to their business owner clients now and not later.

Note: Paris Aden is the founding partner of Valitas Capital Partners, a M&A Advisory Business based in Toronto, Canada. TEC Canada published Mr. Aden’s article. TEC Canada facilitates the formation of business owner peer groups supported by one-to-one coaching, expert speakers, education and global networking.

I suggest the number one ‘right’ question business owners and their advisors need to ask today is: Does your business currently have a strong enough balance sheet to enable it to survive and prosper through at least two years of recession?

Prior to readers answering that question in the context of any given business, I further suggest they focus and reach conclusions on the following supplemental questions:

Does your business have unused borrowing capacity available if funding to bridge a business downturn is required?

Does your business own assets redundant to its operations that could be liquidated if necessary?

Can your business significantly improve its operating discretionary cash flow by achieving labor, material, overhead or other cost savings within its current cost structure?

Does your business have well-maintained capital equipment that will not necessitate large capital expenditures in the foreseeable future as a result of un-remedied wear and tear?

Irrespective of the state of maintenance of the current capital equipment of your business will your business likely face major capital equipment requirements as a result of ongoing technological advances?

If your business is likely to face technology-related major capital equipment requirements is the timing of that spend going to occur earlier than you previously anticipated?

Does your business have significant contingent environmental, unfunded pension or other liabilities that may negatively affect its long-term viability?

Is your business subject to declining operating margins and after-tax discretionary cash flow in an increasingly competitive business environment?

Answer/Commentary

In our current and prospective economic, business and societal environment for most businesses continual review of balance sheet strength needs to be a, if not the top business owner priority. This where balance sheet strength at any given point in time means in:

the first instance that a business has an adequate yet efficient level of working capital to meet its business plan.

the second instance means that a business is not over-levered. That is, the business does not owe more than an appropriate amount of third-party interest-bearing debt given its asset base and its current and expected annual operating before- and after-tax discretionary cash flow.

the third instance ensuring a business is financially positioned to be able to survive significant both anticipated and unanticipated external and internal economic, industry, and company-specific events.

In our current environment, I suggest the importance of balance sheet strength can’t be underrated. This given prevailing economic, business and financial markets uncertainty that follows from, along with other things:

We have not experienced a period of recession (defined by economists as two consecutive quarters of gross domestic product growth decreases) in most of the developed countries for over a decade. It is virtually certain that we will face recession at some point. This where history and current economic indicators suggest for many that recession will come sooner than later, but inevitably will come.

Ongoing globalization issues, threats of de-globalization, continual government bickering over and disruption to international trade agreements and tariffs – principally emanating from the U.S. Oval Office policies, arguably have taken on a life of their own.

Increasing evidence that Central Bank so-called quantitative easing policies introduced in and after 2008 are not generating central bank anticipated economic growth in many countries.

The U.S. currently accounts for about 25% of world gross domestic product. Disruptive and polarized U.S. politics and polarized international and national policies largely emanating out of the White House, combined with the continual “Mueller cloud” that hangs over Mr. Trump’s Presidency, are economically and societally disturbing within the U.S. and elsewhere.

Government debt in many developed countries including the U.S. and Canada continues to escalate with no end in sight. I suggest that in particular this cumulative debt escalation, required infrastructure updates, climate change, and escalating societal issues inevitably must result in increased government regulation, increased business taxes, and other increased monetary levies on both privately- and publicly-held businesses.

Business consolidation in most industries continues apace. this threatens many smaller companies as large companies enjoy efficiencies as a result of critical mass, changes to supply (inputs) and distribution chain management, and a greater opportunity than smaller companies will have to exploit new and advancing technologies to their advantage.

Ongoing technological advances that many believe will result in significantly increased unemployment and societal disruption. If you haven’t read the 2013 Oxford University Study titled The Future Of Employment: How Susceptible Are Jobs To Computerization I suggest you do that.

An environment where if financial institutions were deemed ‘too big to fail’ in 2008 they are in 2019 even bigger and more influential. This where those financial institutions influence, if not as a practical matter control – the equity trading and investment markets.

In summary, I suggest business owners need to focus on the current and prospective efficacy of the balance sheet of their respective businesses – preparing for the worst while hoping for the best.

Here is an what I consider to be a critical early question that I ask of business owners about their business when discussing its value and ownership transition.

The Right Overview Business Transition Question

Do you believe one or more of the following things – either individually or in combination – Is going to result in a material positive, neutral, or negative impact on your business in the contexts of (a) its viability as a going concern and (b) its value growth potential:

ongoing globalization?

prospective central bank policies, particularly ongoing policies and practice of the U.S. Federal Reserve – this where the U.S. economy currently accounts for about 25% of world gross domestic product?

current and prospective government debt and business-related regulations and Interventions?

macro-, country-, and region-specific economic trends?

ongoing technology advances?

business combinations in your industry(ies)?

should you as a business owner and your business consultants be focused on these things to a greater degree than they are when contemplating business value and transition?

Overview Commentary – Business Transition

In discussion with business valuation consultants, I have found most address these things – albeit not always in the depth or risk-related concern I believe is appropriate.

On the other hand, and where this may be somewhat unfair, I have found many persons I have interacted with who hold themselves out as business transition consultants – particularly those who principally offer what I refer to as soft-side transition advice – tend not to focus on these and other business issues to the degree I believe they should as they focus on things such as the importance of good communication among owners. Those things said, the questions posed in this post are for me taking on ever-increasing importance in the context of both business value and transition. This in an economic and business environment where many are expressing increasing concern over world and country-specific economic growth, financial markets volatility, trade protectionism, ever-increasing government debt and regulation, ongoing and potentially disruptive technological advances, ongoing climate change, apparent increasing societal disorder in many countries, and ongoing U.S. political partisan behavior.

RSS - Posts

RSS - Posts